Most PE firms still diligence federal contractors the way they did in 2010. A walkthrough of what the modern version looks like, phase by phase.

Most private equity firms have at least one defense or federal services name they've walked away from in the last two years. Not because the deal was bad. Because the diligence timeline didn't fit the process, the market sizing came back soft, and the committee couldn't get comfortable with the recompete exposure in the time available.

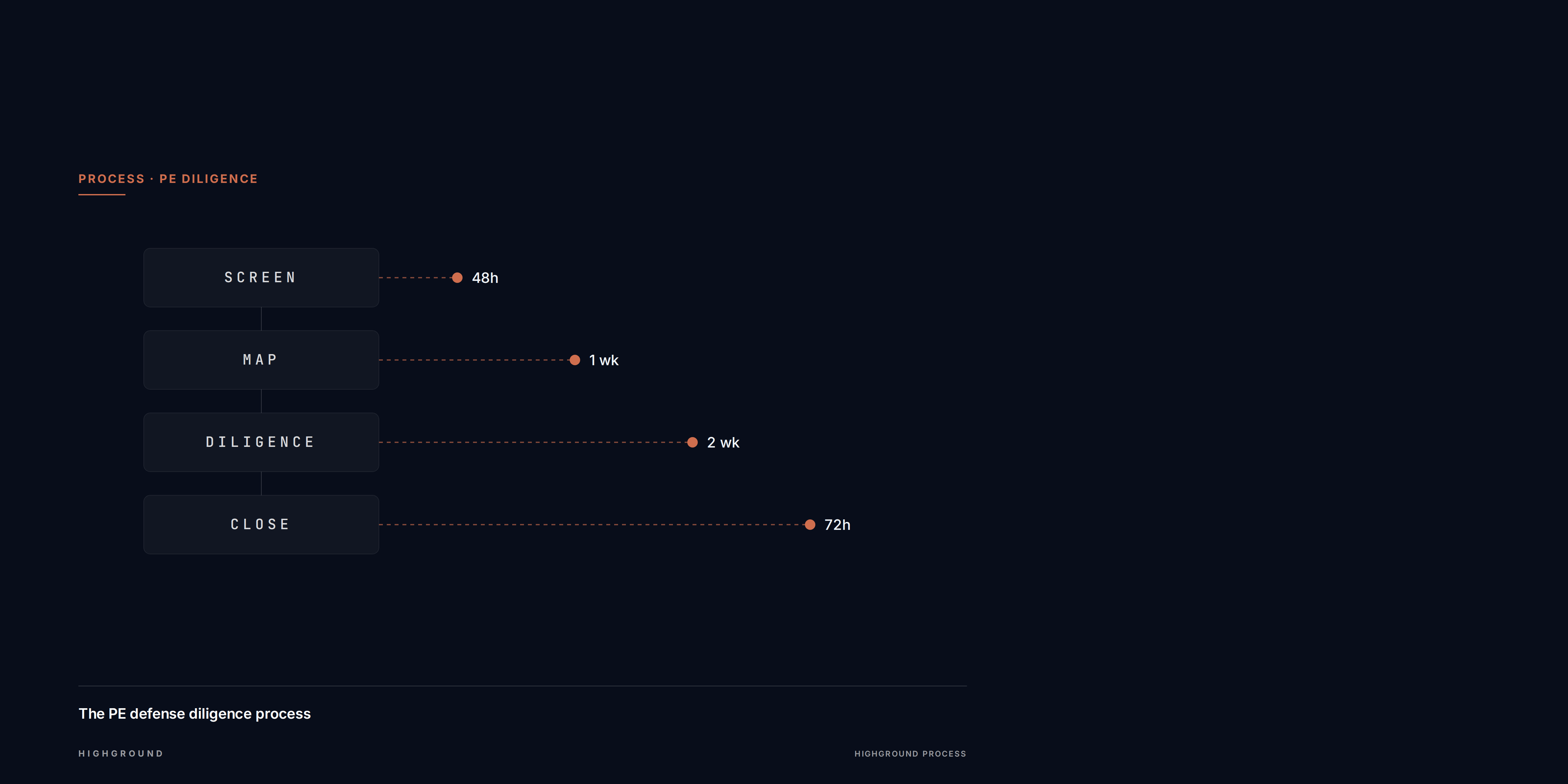

That pattern is changing. A handful of firms have rebuilt their federal diligence process around data and AI, and they're closing deals in a fraction of the time their peers need. What follows is a phase-by-phase walkthrough of how that process actually runs on a defense contractor acquisition.

Deploying capital into the federal supply chain should be easier than it is. Three barriers keep getting in the way.

Fragmented data. The information needed to underwrite a federal deal lives across FPDS, USAspending, SAM.gov, congressional marks, J-Books, subaward networks, and a dozen smaller systems. Reconciling them manually burns the first two weeks of every process.

Slow, partial diligence. Even with that effort, most diligence decks close with caveats. "Market sizing based on available data." "Recompete exposure difficult to confirm." "Growth assumptions subject to budget visibility." The hedges are there because the underlying analysis couldn't be pushed further in the time available.

Poor timing visibility. Procurement cycles, budget flows, and appropriations don't move on calendar quarters. Firms without clear visibility into when capital actually obligates miss windows that determine whether a thesis works or doesn't.

The cumulative effect is that firms either avoid the sector entirely or accept lower risk-adjusted returns on the deals they do execute. Both are suboptimal. Both are now solvable.

The first question on any federal deal is whether the underlying market is large enough and predictable enough to support the thesis. In a traditional process, that question takes two to three weeks to answer properly.

In a modern process, it takes an afternoon. The analysis includes market sizing across relevant agencies, historical award records with values and durations, TAM segmented by the target's core competencies, competitive intensity across the contract base, and a contract waterfall projecting three-to-seven years of revenue visibility from the existing book.

The output isn't a pitch document. It's a decision: does this target sit in a market large enough and stable enough to justify deeper work. Firms using modern intelligence get to that decision fast enough to pass on bad deals before they've burned a week of associate time.

Once the market clears, the next question is whether the margin profile is real. Federal services and defense businesses run on contract structures that most commercial operators don't encounter. Cost-plus, T&M, and FFP vehicles each carry different margin dynamics, and the mix across a contractor's book tells you more about the business than any EBITDA bridge.

Modern diligence breaks the portfolio down across contract types, surfaces the profitability patterns that drive actual operating margin, and benchmarks revenue per employee against industry peers. The output is specific: here are the levers that would move margin post-close, and here are the ones that look attractive in the model but don't hold up against the data.

That level of specificity is what separates a defensible valuation model from a speculative one.

This is the phase that kills the most federal deals, and it's the phase where traditional diligence is weakest.

Every federal services business sits on a book of contracts with finite terms. Some will recompete. Some will be consolidated into larger vehicles. Some will go away entirely when a program office shifts priorities. The question isn't whether the book will turn over. It's which specific contracts are at risk, when, and how the target has historically performed on recompetes.

Modern diligence answers that directly. Competitive positioning for every upcoming recompete. Contract expiration mapping across the next twelve to thirty-six months. Historical recompete win rates broken out by contract type and customer. The output is a quantified revenue cliff analysis, not a qualitative "management is confident in renewals" paragraph in the diligence report.

Firms running this level of analysis are the ones that actually see the cliff before they sign the SPA.

The growth story is where most federal deals get mispriced. A target walks into a process with a plan to expand into three adjacent agencies over the hold period. Commercial diligence tools can't tell you whether that plan is grounded in anything real.

Modern federal intelligence can. Adjacent agency and whitespace analysis shows where the target's capabilities actually match unmet demand. Capability-to-demand matching aligns the growth thesis against upcoming requirements. Congressional mark activity confirms whether the funding the plan depends on is actually moving through appropriations. Competitor expansion benchmarks show how similar moves have played out historically.

The output isn't approval or rejection of the growth plan. It's a revised version of the plan, grounded in what the data actually supports, that the firm can underwrite with conviction.

Four phases. Each compressed from weeks to hours. None of that matters on its own.

What matters is the second-order effect. Firms running modern federal diligence process more deals per quarter, with higher conviction on the ones they pursue, and with clearer visibility into the risks they're actually taking. That translates into better deal selection at the top of the funnel, tighter pricing discipline at the close, and more durable returns across the hold period.

The gap between firms that have made this shift and firms still running 2015-era diligence is already showing up in the win-rate data. It will show up in the return data next. Federal markets reward the firms that can read them clearly, and the tools for reading them clearly are no longer scarce. They're just unevenly adopted.

The firms that adopt first will spend the next five years buying assets the rest of the market can't properly price. That's the real competitive advantage. Everything else is a feature list.

No cadence. No fluff. Original analysis on government demand, defense procurement, and federal capital movement, sent when we have something worth reading.

For PE, VC, sell-side, BD, capture, and strategy teams covering defense.