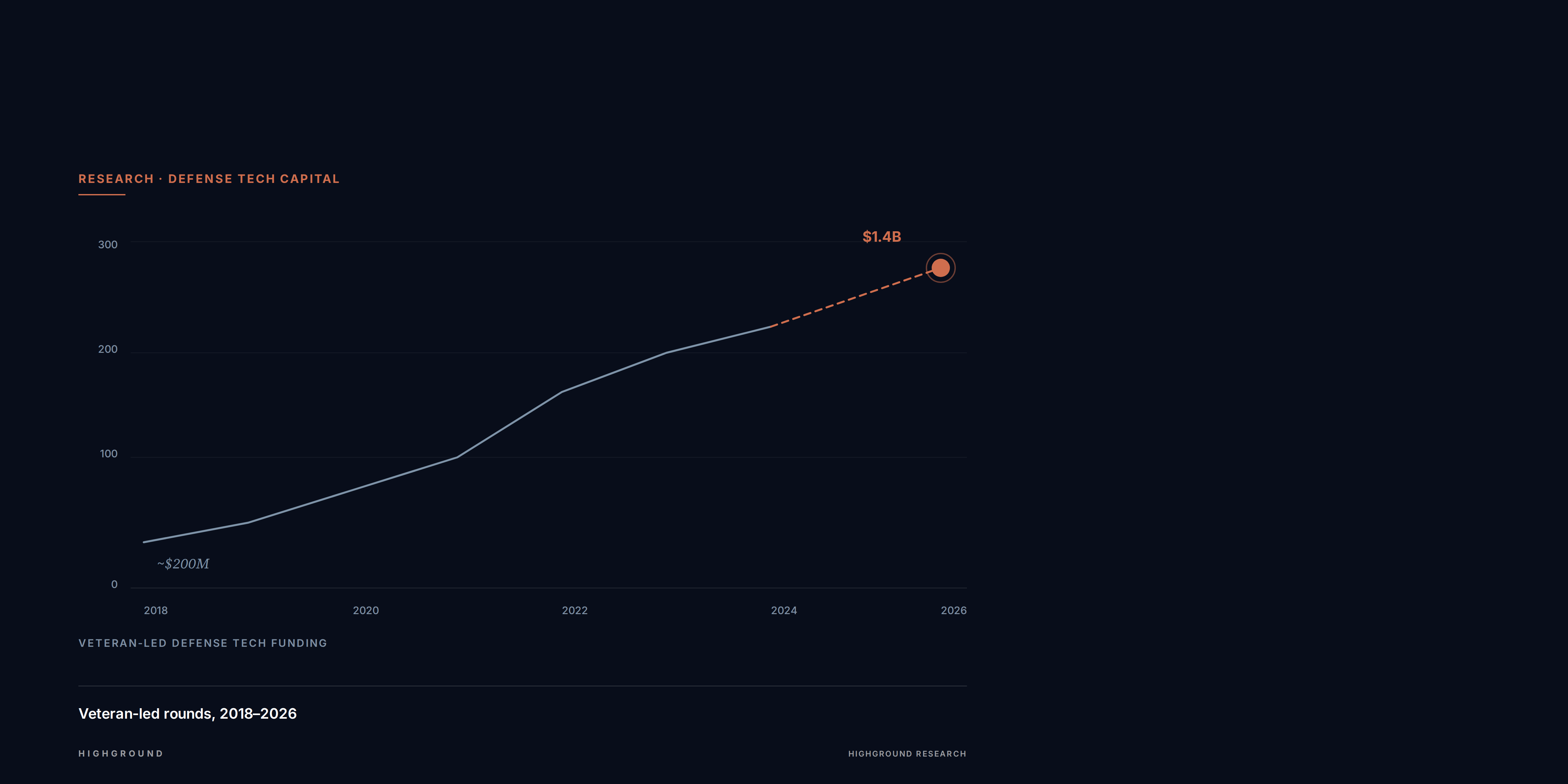

Veteran founders just raised over $1.4 billion across eight rounds. The pattern isn't about narrative or patriotism. It's about where defense tech alpha actually lives.

Eight rounds. Eight veteran founders. More than $1.4 billion in new capital, most of it landing in the last several weeks.

Saronic closed $600M. Epirus closed $250M. True Anomaly added $260M. Shield AI pulled down another $240M. The rest of the list, Allen Control Systems, Vatn Systems, Rune Technologies, Dunedain, stretches from Series A down to pre-seed. The spread matters as much as the total. Capital isn't flowing to one stage or one category. It's flowing to a profile.

That profile keeps repeating: former operators building for operators, backed by investors who have stopped treating defense as a specialty corner and started treating it as one of the highest-signal categories in venture.

Andreessen Horowitz, Sequoia, General Catalyst, and Context Ventures are writing the biggest checks, and they're writing them earlier in the cycle. The thesis behind those decisions is narrower than it first appears. It isn't about resilience or leadership or any of the softer narratives that get attached to military service. Those qualities matter at the margins. They aren't what moves a term sheet.

What moves the term sheet is operational leverage. Veteran founders shorten every expensive part of a defense company's lifecycle.

Requirements discovery that normally takes eighteen months collapses into weeks, because the founder already knows what the end user actually needs and, more importantly, what they've tolerated because nothing better existed. Procurement pathways that require an entire BD function to learn are already internalized. Program-office relationships that take years to build are carried in from day one. Product-market fit is less a hypothesis and more a memory.

That compounds. By the time a non-veteran-led competitor has figured out the customer, the veteran-led one has already shipped, iterated, and started winning recompetes.

The defense market looks like commercial software from a distance and nothing like it up close. Buyers have budget cycles that don't align to calendar quarters. Adoption requires satisfying requirements that aren't written down anywhere public. The person who writes the check is usually three organizational layers away from the person who uses the product.

Founders who came out of uniform know this in their bones. They price their contracts for the actual obligation profile, not the advertised one. They build for the end user's real workflow, not the sanitized version in an RFP. They know which program offices are about to consolidate and which are about to fund. That kind of knowledge doesn't show up on a pitch deck. It shows up in how fast the company closes its first five contracts.

The recent rounds aren't spread randomly. Six categories are pulling disproportionately.

Autonomous systems. Air, ground, and maritime. Saronic's $600M and Shield AI's $240M both land here. The thesis is that uncrewed platforms reduce risk to personnel while expanding the force structure, and the operational demand signal from recent conflicts has been unambiguous.

Directed energy. Epirus at $250M. Counter-UAS has moved from emerging category to urgent requirement in eighteen months, driven by drone threats across multiple theaters.

Space security. True Anomaly at $260M. The orbital domain is the most contested it has ever been, and the acquisition timelines for commercial space capability have compressed faster than anyone predicted in 2022.

Counter-UAS, military logistics, and advanced manufacturing round out the spread. Each is backed by specific policy signals: the FY24 NDAA authorized $874B in total defense spending, the Defense Innovation Unit reports commercial technology adoption inside the DoD has accelerated 35% since 2021, and NATO budget commitments have reversed a three-decade drawdown.

This isn't one sector getting hot. It's a category repricing.

The veteran-founder concentration is a leading indicator, not a story. It tells you that the operators closest to the problem are building the companies, and the investors closest to the data are funding them earliest.

The implication for anyone underwriting defense exposure is straightforward. The signals that actually predict which of these companies become durable platforms aren't in press releases or conference rosters. They're in the federal data itself. Obligation patterns. Recompete cycles. Program-office movement. Subaward networks. Congressional mark activity.

The firms reading those signals are writing Series A checks at prices that will look like theft in three years. The ones still relying on secondhand intelligence will be buying growth-stage positioning at a multiple of today's pricing.

Veterans aren't winning because the market is being polite. They're winning because they got there first and the data says they're going to stay there.

No cadence. No fluff. Original analysis on government demand, defense procurement, and federal capital movement, sent when we have something worth reading.

For PE, VC, sell-side, BD, capture, and strategy teams covering defense.